Business credit scores hold a crucial influence over the financial stability of any small business. They impact various aspects, from acquiring loans and negotiating favorable terms with suppliers to drawing the attention of prospective investors. Many business owners find the nuances of credit scores intimidating, yet grasping these details is vital for making smart financial choices. With a solid understanding of how business credit scores work, entrepreneurs can position their businesses for success and confidently chart a course toward future growth. By mastering the dynamics of credit scores, you equip your business with a powerful tool for thriving in a competitive marketplace.

Understanding Business Credit Scores

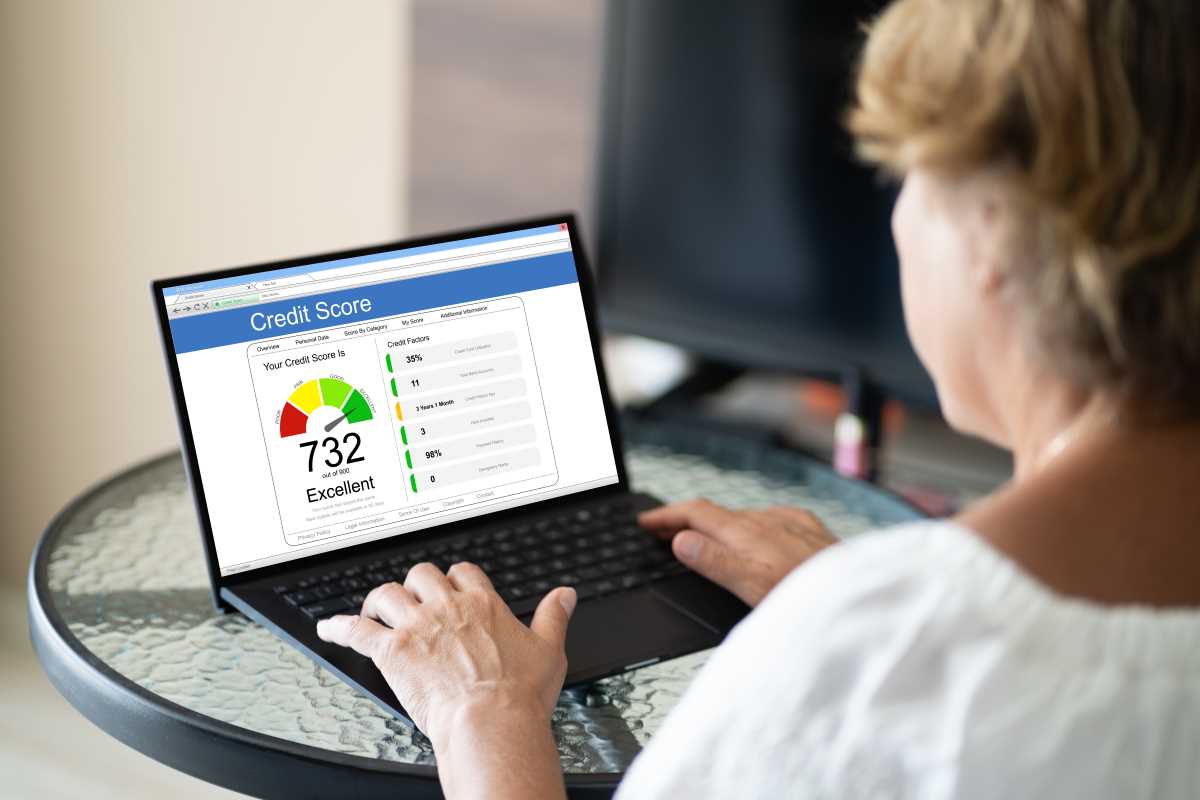

Business credit scores represent a company's creditworthiness, much like personal credit scores indicate an individual's financial reliability. These scores help lenders, suppliers, and partners evaluate the risk of engaging in financial transactions with your business. Here are the key factors that influence business credit scores:

- Payment History: Timely payments on loans, credit lines, and vendor accounts are crucial. Late payments can significantly damage your score.

- Credit Utilization: The ratio of your current outstanding debts to the total available credit. Lower utilization rates generally yield better results.

- Length of Credit History: The longer your business has been managing credit, the more data exists to assess your reliability.

- Public Records: Bankruptcies, liens, and judgments negatively impact your credit score.

- Industry Risk: Some industries have a higher risk than others, affecting your business credit evaluation.

Assessing Your Current Credit Score

Before you can improve your business credit score, you must know where you stand. Here’s how to check and interpret your current business credit score:

- Obtain Your Credit Reports: Start by requesting your business credit reports from major credit bureaus like Dun & Bradstreet, Experian, and Equifax.

- Review the Information: Look for accuracy in your business information, including your company's name, address, and credit history. Discrepancies can affect your score.

- Understand the Score Components: Familiarize yourself with what contributes to your score, such as payment history and credit utilization.

- Identify Areas for Improvement: Highlight any negative factors or inaccuracies that need addressing to improve your score.

Building a strong financial safety net is essential as it provides a buffer that can help maintain your credit health during unexpected challenges.

Steps to Improve Your Business Credit Score

Improving your business credit score involves consistent effort and careful planning. Here are effective steps you can take:

- Make Timely Payments: Ensure all your business accounts are paid on time. Late payments can severely impact your credit score.

- Reduce Debt Levels: Keep your credit utilization low by paying down existing debts and avoiding the accumulation of new ones.

- Establish Trade Lines: Build relationships with suppliers and vendors by establishing trade lines that report to credit bureaus.

- Separate Personal and Business Finances: Use dedicated business banking accounts to prevent mixing personal and business expenses, which can complicate credit assessments.

- Increase Available Credit: Request higher credit limits from your lenders to improve your credit utilization ratio, provided you can manage the increased credit responsibly.

- Regularly Monitor Your Credit Reports: Stay informed about your credit status by regularly checking your business credit reports for accuracy and updates.

- Address Negative Items: Take proactive steps to resolve any outstanding debts or errors that may be dragging down your score.

By focusing on improving your credit score, you can enhance your business's financial standing and open doors to better opportunities.

Common Mistakes to Avoid

Managing your business credit score effectively also means avoiding common pitfalls that can harm your score:

- Ignoring Your Credit Reports: Failing to regularly check your credit reports can allow inaccuracies or negative items to go unnoticed.

- Mixing Personal and Business Finances: This can lead to confusion and negatively affect your business credit profile.

- Overextending Credit: Taking on more credit than your business can handle can strain your finances and damage your credit utilization ratio.

- Closing Old Accounts: Length of credit history matters. Closing old accounts can shorten your credit history, potentially lowering your score.

- Not Addressing Delinquencies: Letting late payments or defaults linger without addressing them can have long-term negative effects on your score.

Monitoring and Maintaining Your Credit Score

Keeping a close eye on your business credit score is essential for maintaining a healthy financial profile. Regular monitoring allows you to catch and address issues early, ensuring your credit remains in good standing. Here are some tools and services that can help:

- Credit Bureau Services: Subscribe to monitoring services offered by credit bureaus like Dun & Bradstreet or Experian to receive updates on your credit status.

- Financial Software: Utilize financial management tools that integrate credit monitoring features to stay informed about your credit health.

- Alerts and Notifications: Set up alerts to notify you of significant changes or activities related to your credit reports.

- Professional Assistance: Consider working with financial advisors or credit consultants who can provide expert guidance and support in maintaining your credit.

By diligently monitoring your credit score, you can make informed decisions and take timely actions to sustain a strong business credit profile.

Maintaining a solid business credit score involves continuous attention and proactive management. By understanding influencing factors, assessing your score, implementing improvements, and avoiding mistakes, you position your small business for financial success and growth.

.jpg)

.jpeg)